Why Malaysia Matters More Than Its Size Suggests in SEA SaaS

Malaysia is only 10% of SEA's SaaS market, but the smartest second move after Singapore. English fluency, MD Status perks, and Singapore overflow explain why.

Most global SaaS treat Southeast Asia as Singapore plus Indonesia plus other countries. The hierarchy is completely wrong and it needs to be fixed.

We know that Malaysia with estimated population of 36.4 million is slightly smaller than a city in Indonesia where Jakarta metropolitan itself has an estimated population of 42 million.

There are three reasons to compound with Malaysia. English fluency at scale, regulatory openess for foreign technology and a regional HQ in Singapore that's getting increasingly expensive.

None of these reasons make a big impact individually. But putting them all together makes Malaysia the highest leverage second move after Singapore for almost every SaaS expanding into the SEA market.

When was the last time you had your GTM strategies meeting for the Southeast Asia region?

This is the same pattern you may see in every single meeting.

The first priority is always Singapore, positioned as the regional HQ and financial hub, with many expat decision-makers living there.

Next, Indonesia, for its population.

Then Thailand and Vietnam will get the attention for the industrial software plays.

The Philippines, a powerhouse in BPO and other services such as offshore accounting and HR, also draws attention.

And finally, Malaysia will be mentioned with these exact words," and we should probably also look at..."

The priority order for SaaS market expansion in the SEA region is based on these three assumptions that are reasonable but fall apart in practice.

- Assumption 1: Market size determines opportunities. Indonesia has a population of 288.3 million (as of 2026). The Philippines has 117.7 million. Vietnam has 102.2 million. And Malaysia has only 36.4 million. Malaysia is just one-tenth of the entire pie.

- Assumption 2: Singapore is the regional capital and has the capacity to absorb regional functions fully. Build there, hire there, sell from there. Other markets are just secondary, complementing the entire region.

- Assumption 3: Language is less important than purchasing power. English works like a charm for the C-suite anywhere in the region; you don't have to think hard about which country is structurally easier to enter.

These assumptions are positioning Malaysia wrongly within the SaaS expansion market. And before you realize the wrong move, you might have already burned your marketing expansion investment.

This is not because Malaysia is the biggest fish in the pond.

But it's the most informative one.

Just take a look at the foreign direct investment in Malaysia for the last 6 months.

According to MIDA (Malaysia Investment Development Authority), Malaysia recorded the highest FDI inflows in Q4 of 2025 at RM27.28 billion (US$7 billion) and in Q1 of 2026 at RM22.81 billion (US$5.77 billion).

Malaysia acts as a bellwether for the rest of SEA in ways no other market does.

And here's why.

Reason 1: The English language Advantage Isn't about English

EF Education released its English Proficiency Index (EPI) in November 2025.

Malaysia is ranked 24th globally with a score of 581. It is among the highest in Asian countries where English is not the native language. Singapore has been removed from the rankings in 2025 because it's now considered a native English-speaking country.

So, going back to Malaysia. Kuala Lumpur scored 588 as the capital city, also one of the highest in Asia in its category. And the best part is that Penang scored 589, the top regional score within the country.

Comparing that to the Philippines at 569, Vietnam at 511, Indonesia at 468, and Thailand at 416.

The gap isn't marginal.

It's structural.

And most SaaS companies miss their mark on GTM strategy for SEA; English fluency in Malaysia doesn't just mean sales reps can pitch in English.

It goes beyond that.

Let's explore them.

Marketing Efforts Convert without Translation

The same sales copies and materials that work in Singapore work in Malaysia at roughly equivalent rates. You don't have to create a full-fledged Bahasa Malaysia translation of the website to convert SME buyers.

Bahasa Malaysia gets you there.

English gets you the sale.

No study measures how English sales pages convert in Malaysia directly, but there is some evidence that I've gathered:

- Malay content earns trust and widens the top of the funnel, which is important for the mass-market SME plays.

- For B2B SaaS, English is the workhorse. Localization is what matters to show that we are here in Malaysia, fully supporting you. That credibility and trust signal matter the most.

Product Documentation Works As It Is

The highest hidden cost of expanding into non-English-speaking countries like Indonesia or Vietnam isn't marketing.

It's the document and knowledge base.

Every help article, onboarding flow, and error message has to be localized for those markets where the buyer might be comfortable in English, but the daily users aren't.

This is where Malaysia largely sidesteps.

English Competency with Global SaaS Team

Your local hires in Malaysia can write in the same English that your global team uses.

This sounds trivial until you've tried to scale a content marketing team across a region where the regional content lead can read your emails and chat conversations, but is unable to write a publishable LinkedIn post in your tone.

Can you relate to this?

Malaysian marketers, writers, and customer support reps can get it done.

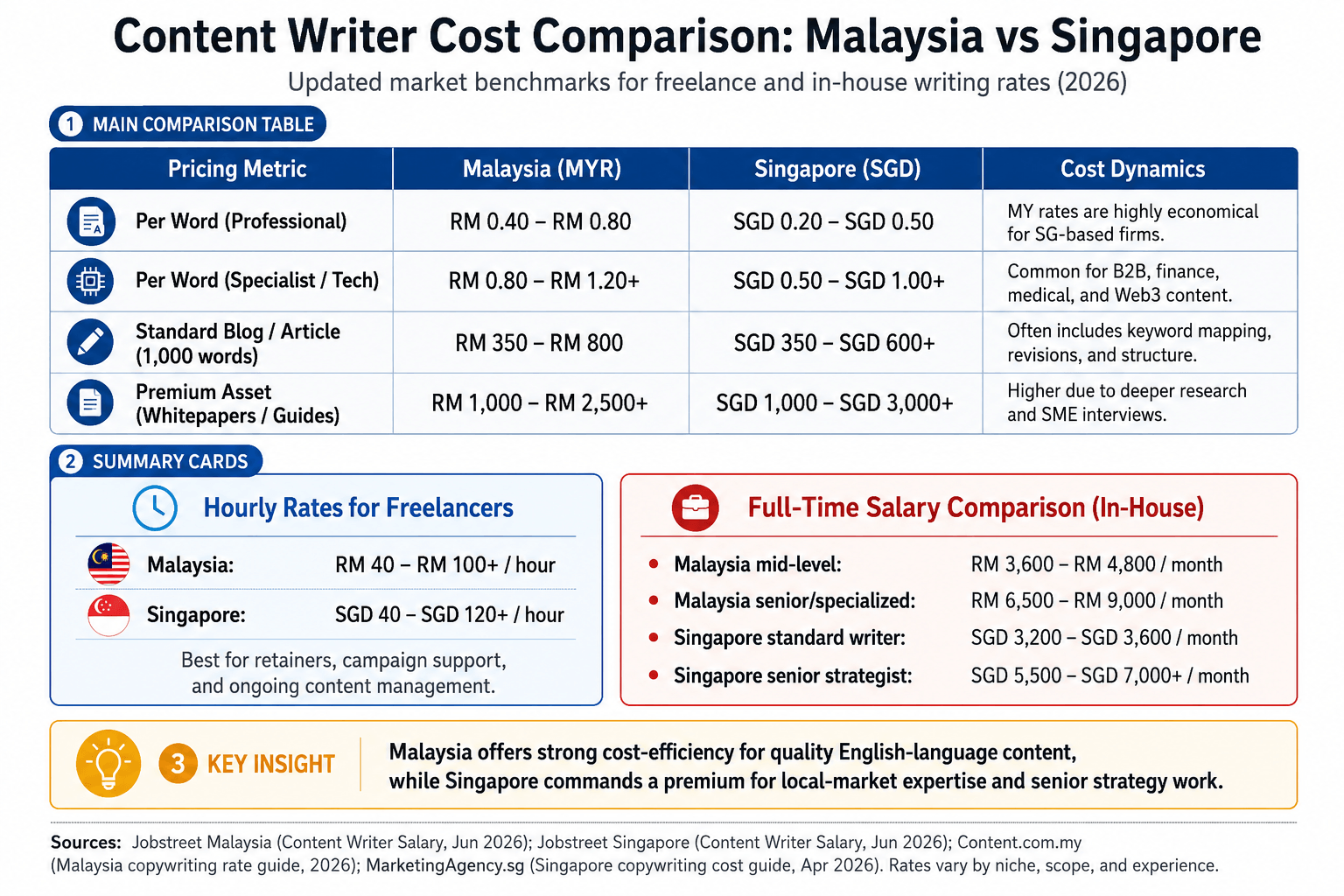

The cost of running a regional content function out of KL is roughly 40-60% of the equivalent in Singapore.

And the output quality is comparable. You can also expect the output volume to be higher, since you can easily hire two or three Malaysians for the cost of one Singaporean.

Read more: Why Malaysia is Central to Global Mobility in 2026

When you understand these factors, you can easily see why Malaysia emerges as the regional content hub for SaaS companies that started in Singapore.

Singapore still keeps the regional sales hub.

But the regional content, regional support, regional marketing ops, and increasingly a regional partnership hub work well from Malaysia.

The English advantage has become more important than ever in operational economics, not just for customer-facing activities.

Reason 2: Regulatory Openness with Infrastructure Backing

Most countries say they want to attract foreign tech investment.

Do you know that Malaysia has spent almost 30 years quietly building the infrastructure to absorb it?

The MSC Malaysia program was launched in 1996.

It was then rebranded as Malaysia Digital (MD Status) in July 2022 and is run by MDEC (Malaysia Digital Economy Corporation).

The current iteration moved from a location-based model to an activity-based one. Initially, you needed to be in Cyberjaya, but now you can be anywhere in Malaysia as long as you're doing the right kind of work.

In January 2026, MDEC added MD Location Recognition. They are offering extra incentives for companies in Malaysia Tech, such as Cyberjaya, Penang, and parts of the Klang Valley.

What Does an MD Status Give a Foreign SaaS Company Expanding into Malaysia?

- Tax Exemption: Up to 10 years, depending on activity tier and investment size.

- Employment: Pre-approved employment quotas, streamlined Employment Pass process.

- Multimedia Operating Freedom: Foreign equity ownership allowed at 100% in qualifying activities.

- Digital Grants: Eligibility for the Malaysia Digital Acceleration Grant (MDAG) that focuses on commercialization and regional expansion.

- Access to MDEC's Partner Network: Expand connections into GLCs, SMEs, universities, and government agencies.

The last one is the most underrated.

As of May 2026, MDEC has close to 900 employees. The main function of MDEC is to connect foreign tech companies to Malaysian buyers and partners.

It's not a passive grant-giver like most people think.

It's an active matchmaker.

Singapore has EDB (Singapore Economic Development Board), similar to MDEC. But Singapore's tax model is built on attracting capital, not subsidizing operations.

This means the effective rate after incentives is still higher than in Malaysia.

Indonesia has the BKPM (the Ministry of Investment and the Ministry of Industry) and sector-based incentive programs. Regulatory complexity, foreign ownership restrictions in many sectors, and frequent changes in requirements can make the game hard.

Vietnam offers industrial park incentives, but incentives for SaaS-focused companies are limited. And Thailand offers BOI incentives, but it is increasingly cost-competitive compared to other ASEAN countries.

Malaysia is not entirely about tax exemption.

It's about tax exemptions, infrastructure, English-speaking talents, regional connectivity, and a government agency focused on helping you succeed locally.

That's completely a different value proposition.

We can clearly see it in the recent expansion of global companies like Alibaba Cloud, which is establishing a second regional hub in KL, AWS's data center investment, and Microsoft's aggressive expansion in 2025-2026.

And most mid-market SaaS companies are increasingly choosing Malaysia as their first regional operations base, as Singapore is more expensive now.

That's what we'll cover next.

Reason 3: The Singapore Overflow Effect

All of us know that Singapore is the regional HQ for both global and Southeast Asia SaaS companies. In the first half of 2025, Singapore captured almost 92% of Southeast Asia's total startup funding and 88% fintech funding.

This is the country where the term sheets are signed, where the regional managing directors sit, and where international banking takes place.

No one disputes this.

But a few things started to fall apart.

Singapore has gotten too expensive to absorb regional operations beyond a certain headcount.

The numbers are widely available.

But...

- A mid-level marketing manager in Singapore costs roughly SGD 8,000-12,000 per month.

- A content writer costs SGD 5,000-7,000 (median).

- Office space in CBD areas ranges from SGD 12 to SGD 18 per square foot per month.

- A startup with 30 employees in Singapore can easily burn SGD 250,000-400,000 per month on operating costs alone, without any product spend.

Most regional SaaS companies reach a threshold of around 15-25 employees. That's when they start keeping only the executive team and the finance function in Singapore.

Everything else is being repositioned in different countries within the SEA region.

The natural overflow goes to one of these three places:

- Kuala Lumpur - marketing, content, partnerships, mid-market sales, customer success, and regional ops.

- Manila - support and operations

- Bangalore - for engineering and technical support (this is exceptional)

Why did KL win this allocation more than the other two locations?

- Time overlap with other countries in SEA: Singapore (0 hours), Hong Kong (0 hours), Jakarta (1 hour). Bangalore is 2.5 hours behind. Manila has the same time zone but has historically been a BPO-heavy market.

- Geographic proximity: 45 minutes flight from Singapore, multiple daily flights. Easier for executive visits compared to Manila, where the airport experiences have their own deterrent.

- Cost: roughly 50-60% of Singapore for equivalent talent. Manila is cheaper, but typically, the cost of seniority or English-writing quality. Bangalore is cheaper but doesn't fit non-engineering roles.

- Cultural overlap: Malaysian business culture sits comfortably between Singapore's structured formality and the broader region's relationship orientation. Singaporeans visiting KL find it familiar; Indonesians do as well. It's a hinge market.

These reasons show why almost every SaaS company that scaled beyond Singapore as its only base also built its footprint in Malaysia within 24 months.

In December 2025, Fingular, a fintech SaaS holding company headquartered in Singapore, opened a new hub in Kuala Lumpur as part of its global expansion. The hub is primarily built to host part of its growing team and to be accessible to staff across the organization, including people flying in from other countries to work out of KL.

Zoho is one of the best examples.

In January 2026, it opened a new office in Subang Jaya, Selangor, housing local teams from both Zoho and ManageEngine.

But the stronger signal came earlier.

In 2025, Zoho partnered with Cradle Fund to roll out Zoho For Startups via the MyStartup platform, committing over RM30 million in software support to 3,000 Malaysian startups. A global SaaS player putting real money behind local SMEs, not selling them but equipping them with the right solutions to grow.

Why Malaysia is a SaaS Testing Ground?

Here's the most common part that pricing- and population-focused analysis and research miss.

Malaysia isn't the largest SEA market, and it never will be.

But it's the most representative one.

A country that contains every region of SEA in miniature.

You can't deny this!

Malaysia is a multi-ethnic country in a way no other SEA country quite is. Malay majority (about 70%), Chinese (about 22%), Indian (about 6%), with significantly smaller groups of others. This breakdown is closer to a regionally weighted average than to any single-ethnicity-dominant country in Southeast Asia.

Your buyer behavior in KL gives you a sense of Malaysian Chinese SME behavior, which overlaps structurally with Singaporean, Hong Kong, and Indonesian Tionghoa SME buyer patterns. The Malay buyer behavior allows a preview of Indonesia and Brunei. And of course, Indian buyer behavior overlaps with that of parts of Singapore and the broader diaspora across the subcontinent, such as Sri Lanka.

When we are looking at Malaysia from a religious perspective, the majority of the population is Muslim, with Buddhists, Hindus, and Christians being the minorities. Let's take a look at how it relates to the other countries within the SEA region:

- Indonesia: 87.1% Muslims (approximately 245 million)

- Philippines: 78.8% Christians (approximately 107 million)

- Thailand: 93.4% Buddhist (approximately 66 million)

Malaysia covers all of them on a smaller scale.

If your products need to comply with Islamic finance requirements, Malaysia is the best place to test them before entering the Indonesian market. Malaysia is also your best option to start with if you're selling to a Christian-majority market before targeting the Philippines. If your buyer base is religiously plural, Malaysia can work as your natural sandbox.

You might wonder what religion has to do with the SaaS business. Religion influences the following aspects of a SaaS business:

- Market opportunities

- Organizational ethics

- Pricing models

- Workplace culture

In some scenarios, religious values also influence purchase decisions for SaaS products.

Economically, Malaysia is an upper-middle-income country, with a per capita GDP of around US$13,000 in 2025. It's higher than Indonesia, the Philippines, Thailand, and Vietnam, but lower than Singapore and Brunei.

This is a good example of buying behavior.

Malaysian SMEs aren't price-insensitive like Singaporean SMEs, nor budget-bound like Vietnamese or Indonesian SMEs. They are cost-conscious but willing to pay for quality. Localization still plays a vital role, though they are happy to have the documentation in English.

They may negotiate hard, but once committed, they pay on time.

This mid-tier purchasing behavior among Malaysian SMEs is the closest predictor of how a SaaS product will perform across the upper-middle and lower-upper tiers in SEA.

When global SaaS companies skip Malaysia and go straight to Indonesia after launching in Singapore, they often benchmark against Singapore, which realistically isn't the market that most closely resembles Indonesia.

It's hard to compare apples to apples and expect to scale linearly.

SaaS companies that test Malaysia between Singapore and then move on to Indonesia consistently get the regional read better.

Buyer objections, pricing sensitivity, channel preferences, and support expectations are among the fundamentals that are easier to test on a smaller scale in Malaysia before committing to a larger spend.

Malaysia is not the bigger piece of the pie.

Malaysia is small.

But Malaysia is the country that tells you what the rest of the countries in the region look like.

My Honest Counter-Argument

Let me be transparent here.

Malaysia is not the future of South East Asia's SaaS market.

It's not going to overtake Singapore as the regional capital.

It's not going to overtake Indonesia in market size.

The structural advantages I've listed here are real but bounded.

The domestic market size is genuinely limited

Malaysia accounts for only 10% of the Southeast Asia SaaS market, while Singapore leads with 31%.

Among B2B SaaS decision-makers in Singapore and Hong Kong, these countries will determine deal flows, while Malaysia will only account for smaller SME players.

Political and currency risk is non-zero.

If you've been following the currency trends of Malaysia, you should know that the ringgit hit RM4.74 to the USD at its worst in early 2024. It recovered to RM3.95 in May 2026, but has been slightly volatile.

The volatility is real, and it affects the USD-billed vendor's Malaysian pricing in unpredictable ways. Geopolitical conflicts still affect the Malaysian market, though we have yet to see any negative impact.

The ups and downs of regulatory environments

SST on foreign digital services.

E-invoicing mandates that are still in phases through 2024-2026.

PDPA updates err....

None of these is a deal-breaker, but each adds compliance overhead that simpler markets don't impose.

And one important one that I don't want to miss out.

"We want our data to be in the local data center".

Local competition is real and often underestimated

Malaysian SaaS companies like Carsome, Involve Asia, Easystore, Storehub, Hashmicro, and Lottiefiles are not pushovers.

These local incumbents understand the buyer better than global entrants, who may take several years to do so. Many of these local players have a deeper regional reach than their headcount suggests.

Singapore's gravitational pull is still strong.

Most regional decision still happens in Singapore, as I've mentioned earlier in this article. Malaysia overflows operationally but rarely strategically. A global SaaS company's CMO probably still lives in Singapore, not KL.

That's a real ceiling on Malaysia's role.

None of these invalidates the disproportionate-leverage arguments.

They just bound it.

What You Should Actually Do?

If you're a SaaS company running a regional GTM (Go-To-Market) strategy in 2026, here's the practical translation of everything I've shared so far.

Don't skip Malaysia as a test market

The cost of running marketing campaigns in KL between Singapore and Indonesia is small.

The information gain is large.

Run 6-12 months soft launch in Malaysia before committing to large investments in Indonesia or the Philippines.

You'll gain some solid information and product-market mismatches that would have cost you 20x the investment in countries like Indonesia.

Build a regional content function in Malaysia

The cost savings can be 40%-60% per headcount in Malaysia compared to Singapore. The output quality is at parity for English content.

Singaporeans can manage it; Malaysians can produce it.

This single decision often creates a bigger investment capacity for regional expansion.

Malaysia as your APAC second base for non-strategic functions

Customer support, content development, marketing ops, partnership, and mid-market sales are some of the functions that can be placed in Malaysia.

The Philippines works well for inbound sales and high-volume ticket support. Looking at Enterprise deals and stronger technical support, Malaysia is your ideal choice.

The finance and executive team can always be in Singapore. And engineering can be in Bangalore or in KL, depending on the talent fit.

This split works very well for global SaaS companies expanding into the SEA market.

MD Status before scaling

Apply for an MD status in Malaysia before you scale.

MD status offers grants and tax incentives that serve as catalysts for global SaaS companies seeking early traction. The MDEC's partner community is easy to leverage, and you can get your first few customers from there.

Take the buyer's signal seriously.

Malaysian SMEs are not smaller than Singapore SMEs. They're in different segments with different expectations, where business relationships, cost, and partnership come into play.

Make sure to align your CAC and sales-cycle forecasting to drive a results-driven shift and get your brand messaging right for the Malaysian business market. Treat the shift as a preview of the rest of the SEA market, not as Malaysia-specific noise.

Bottom Line

Let me repeat this.

Malaysia will never be the biggest SaaS market in Southeast Asia.

Most of you might not agree with me on this, and I may sound reserved. But the fact is that Malaysia is not structurally built to become the biggest SaaS market.

But Malaysia is where you need to kickstart your regional SaaS GTM strategies before scaling to other countries within the region.

Malaysia is the country where the English advantage stops being Singapore-only premium and becomes regionally deployable.

It has also improved, becoming a country with regulatory openness, infrastructure improvements, and government partnerships that drive global tech expansion more easily than any other country in the region.

Malaysia has positioned itself as an extension of Singapore, serving as the operational wing to optimize costs and grow strategically within Southeast Asia.

36 million people.

Structural advantages.

Catalyst for expansion and growth in the Southeast Asia market.

Evaluate, analyze, and execute strategically.

Skip it at your cost.